Unlocking Your Savings Potential: Mastering Annual Interest Calculation

Ever wondered how much your savings are truly growing? In the fast-paced world of finance, understanding the mechanics behind your savings account’s growth is paramount. Calculating annual interest isn’t just a numerical exercise; it's about empowering yourself to make informed decisions and achieve your financial aspirations. This article delves into the intricacies of determining your annual interest earnings, providing a comprehensive guide to help you navigate the world of savings with confidence.

Projecting your savings growth involves more than just wishful thinking. It requires a clear understanding of the factors at play, including interest rates, compounding periods, and the principal amount. Whether you're saving for a down payment, a dream vacation, or simply securing your financial future, knowing how to accurately calculate your annual interest is the first step toward achieving your goals.

The concept of earning interest on savings dates back centuries, evolving alongside the development of banking and financial systems. From simple interest calculations in ancient civilizations to the complex algorithms used in modern finance, the core principle remains the same: your money has the potential to earn more money. Grasping this principle and its practical application is essential for effective financial planning.

One of the main issues surrounding interest calculation is the lack of clear understanding among savers. Many individuals rely solely on their bank statements without truly comprehending how their interest is determined. This knowledge gap can lead to missed opportunities for maximizing returns and achieving financial objectives. By taking the time to learn the fundamentals of annual interest calculation, you can take control of your financial destiny.

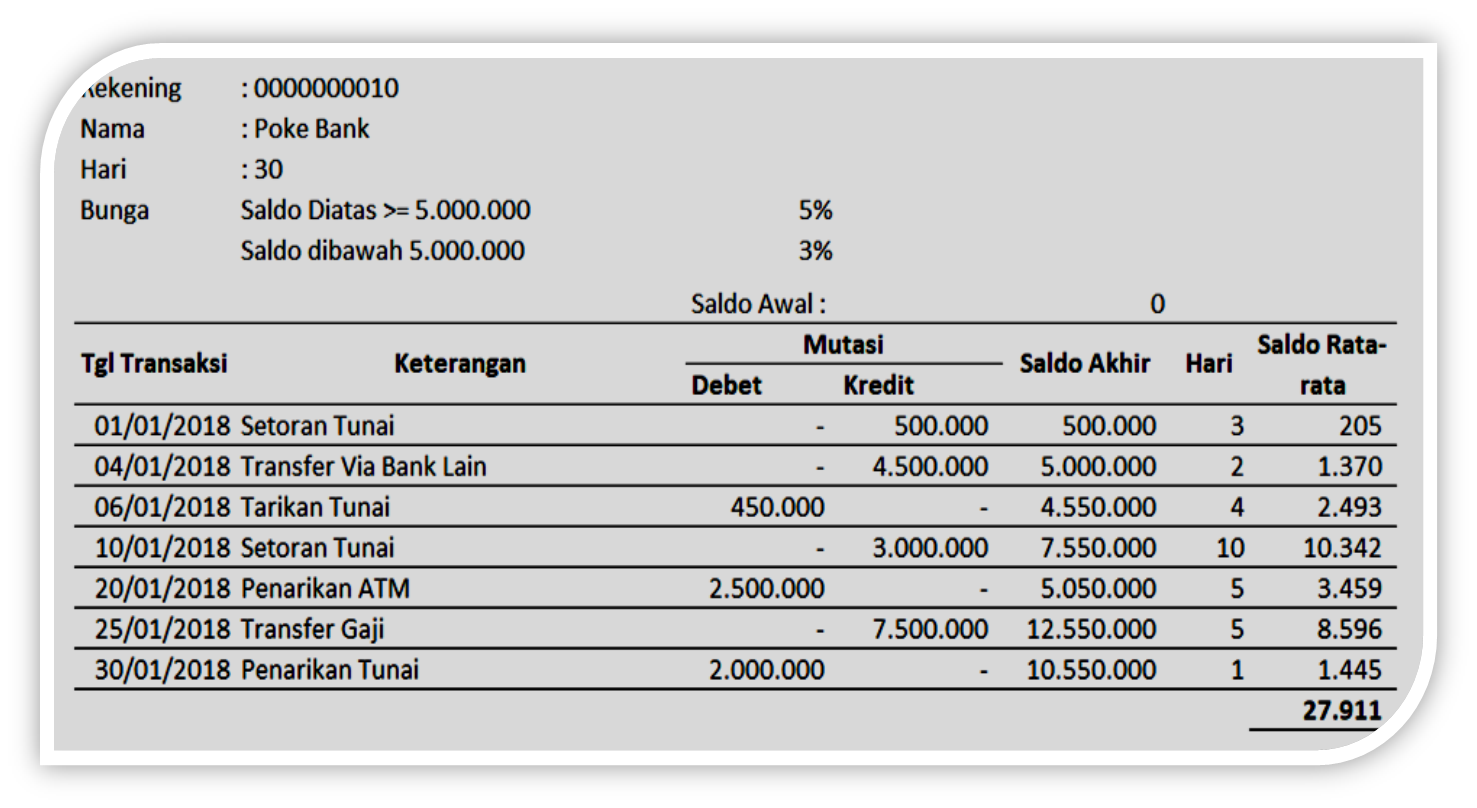

Simply put, annual interest is the amount earned on your deposited funds over a year, expressed as a percentage of your principal. This percentage, known as the interest rate, is a key factor influencing your earnings. Understanding the relationship between the principal, the interest rate, and the compounding frequency is crucial for accurate calculation. For example, a $1,000 deposit with a 2% annual interest rate will yield $20 in interest over a year, assuming simple interest. However, with compound interest, the interest earned is added to the principal, resulting in even greater returns over time.

Let’s delve into the history and origins of interest. Interest has been a crucial element of financial transactions since ancient times, tracing back to civilizations such as Mesopotamia and Babylon. Early forms of interest often involved lending agricultural products with the expectation of receiving a larger return at harvest. Over time, as monetary systems developed, interest became associated with lending and borrowing money. The concept of compound interest, where earned interest is added to the principal, further revolutionized the landscape of finance, amplifying the potential for wealth accumulation. Understanding this historical context allows us to appreciate the significance of interest in modern financial systems.

Calculating annual interest offers several benefits: Firstly, it empowers you to project your future savings and set realistic financial goals. Secondly, it allows you to compare different savings accounts and choose the one offering the best returns. Lastly, it helps you track your financial progress and make necessary adjustments to your savings strategy.

To calculate your annual interest, you need to know your principal balance, the annual interest rate, and the compounding frequency. The formula for simple interest is: Interest = Principal x Rate x Time. For compound interest, the formula is slightly more complex: A = P (1 + r/n)^(nt), where A is the future value, P is the principal, r is the annual interest rate, n is the number of times interest is compounded per year, and t is the number of years.

Here's a simple example: If you deposit $1,000 at a 2% annual interest rate compounded annually, your balance after one year would be $1,020. If the interest is compounded quarterly, your balance after one year would be slightly higher due to the more frequent compounding.

Action plan: Start by gathering your bank statements and noting your current balances and interest rates. Use online interest calculators or the formulas provided to determine your projected annual earnings. Compare different savings accounts and make adjustments as needed to optimize your returns.

Advantages and Disadvantages of Calculating Annual Interest

| Advantages | Disadvantages |

|---|---|

| Informed financial decisions | Requires accurate information |

| Goal setting and tracking | Can be complex with compound interest |

| Account comparison | Doesn't account for unexpected fees |

Five Best Practices: 1. Regularly review your interest rates. 2. Utilize online calculators. 3. Understand compounding frequency. 4. Factor in fees. 5. Adjust savings strategy as needed.

FAQ: 1. What is compound interest? 2. How often is interest typically compounded? 3. How do I calculate interest with varying rates? 4. What are the different types of savings accounts? 5. How can I maximize my interest earnings? 6. What is the difference between APR and APY? 7. How do taxes affect interest earnings? 8. Where can I find reliable interest rate information?

Tips and Tricks: Consider high-yield savings accounts. Automate your savings. Reinvest your earned interest. Take advantage of compound interest. Monitor interest rate changes.

In conclusion, understanding how to calculate your annual interest earnings is a fundamental skill for effective financial management. It empowers you to make informed decisions, optimize your savings strategies, and achieve your financial goals. By actively engaging with the concepts and tools discussed in this article, you can unlock the true potential of your savings and pave the way for a secure financial future. Start calculating your interest today and take control of your financial journey. Don't let your money sit idle; make it work for you by understanding the power of compound growth and maximizing your returns. Remember, financial literacy is not just about numbers; it's about empowering yourself to create a brighter financial future.

Unlock your inner storyteller mga hakbang sa pagsulat for the modern age

Finding comfort and support navigating loss with miles funeral home sterling massachusetts

Unveiling the power of para que sirve el doctorado your guide to success

Cara Menghitung Bunga Tabungan Pelajarindo Com | Solidarios Con Garzon

33 Contoh Soal Mencari Bunga Bank yang Banyak Dicari | Solidarios Con Garzon

Menghitung Bunga Bank Per Tahun | Solidarios Con Garzon

Cara Menghitung Bunga Tabungan Agar Tahu Potensi Untung | Solidarios Con Garzon

cara menghitung bunga tabungan per tahun | Solidarios Con Garzon

Cara Menghitung Suku Bunga Kpr | Solidarios Con Garzon

Cara Menghitung Besar Bunga Pinjaman Bank | Solidarios Con Garzon

Cara Menghitung Bunga Pinjaman Tips dan Trik untuk Menghitung Bunga | Solidarios Con Garzon

Contoh Soal Suku Bunga Tabungan | Solidarios Con Garzon

Cara Menghitung Bunga Per Tahun Matematika Matematika Dasar Images | Solidarios Con Garzon

Cara Menghitung Bunga Tetap Terbaru Viral Gastroenteritis In Children | Solidarios Con Garzon

Pengertian Bunga Bank Jenis dan Cara Menghitungnya | Solidarios Con Garzon

Cara Menghitung Bunga Majemuk Tahunan Terbaru | Solidarios Con Garzon

PT BPR DANAMITRA SURYA | Solidarios Con Garzon

Contoh Soal Suku Bunga Tabungan | Solidarios Con Garzon