Unlocking Healthcare: Your Guide to Medicare Part A and Part B

Are you approaching retirement or already enjoying your golden years? One thing's for sure, healthcare costs can put a serious dent in your hard-earned savings. Understanding Medicare, especially Part A and Part B, is crucial for a financially secure and healthy future. This comprehensive guide will equip you with the knowledge to navigate the sometimes confusing world of Medicare coverage.

Medicare, a federal health insurance program primarily for people 65 and older, also covers some younger people with disabilities or end-stage renal disease. It's divided into different parts, each covering specific services. We'll focus on Medicare Part A, which covers hospital insurance, and Medicare Part B, which covers medical insurance. These two form the foundation of your Medicare coverage and understanding them is the first step towards effectively managing your healthcare expenses.

Medicare Part A and Part B have separate coverage aspects. Medicare Part A covers inpatient hospital stays, skilled nursing facility care, some home health care, and hospice care. Think of it as your safety net for major medical events. Medicare Part B, on the other hand, covers doctor visits, outpatient services, preventive care, and some medical equipment. This is your coverage for routine medical care and helps keep you healthy in the long run.

Medicare has its roots in the Social Security Amendments of 1965, signed into law by President Lyndon B. Johnson. Recognizing the increasing healthcare needs and costs faced by older Americans, the creation of Medicare represented a significant step towards ensuring access to quality healthcare for seniors. Today, Medicare serves millions of beneficiaries, proving its vital role in the healthcare landscape.

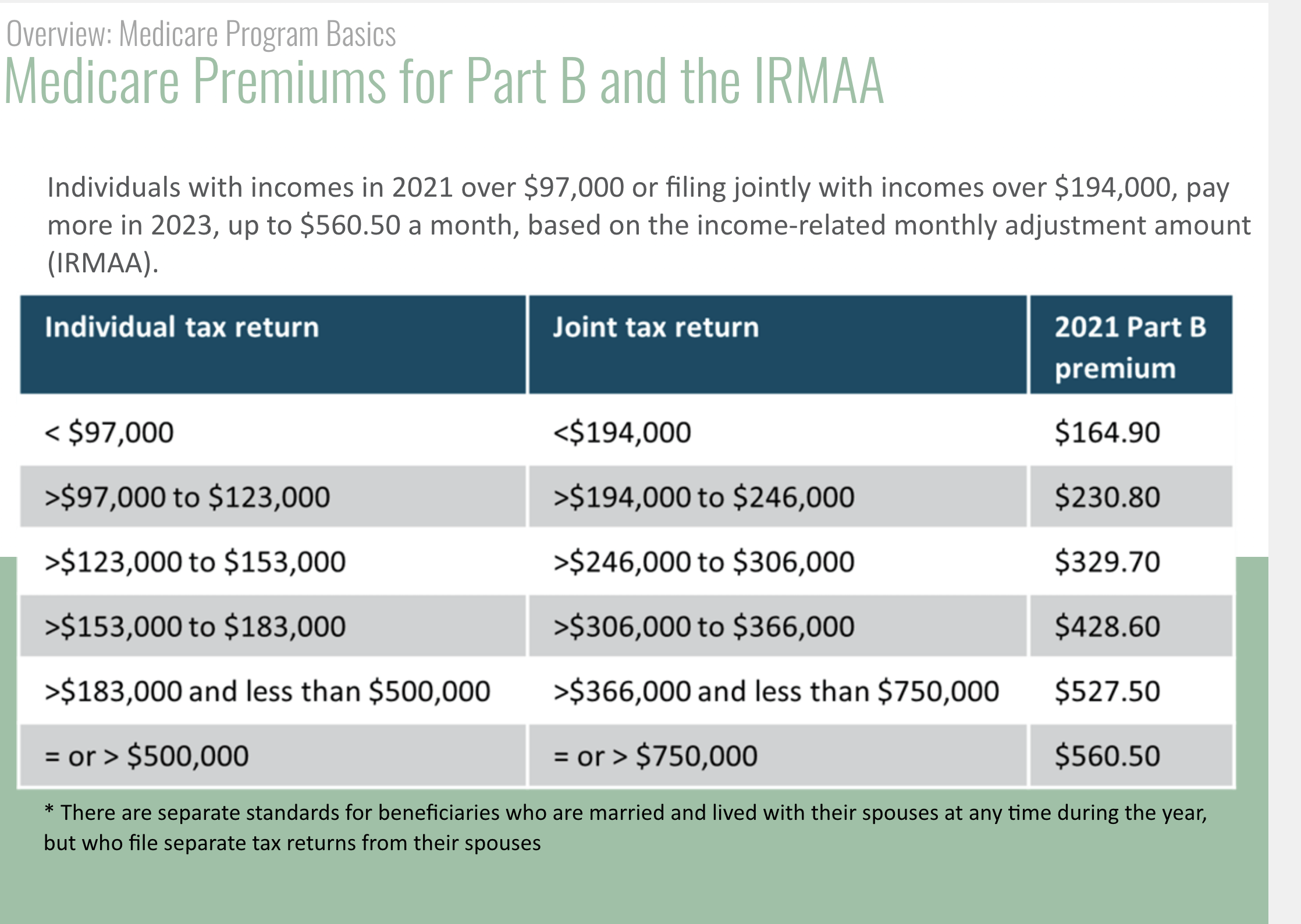

While Medicare Part A and Medicare Part B offer essential coverage, it's important to understand they're not entirely free. Most people qualify for premium-free Medicare Part A based on their work history. However, Medicare Part B usually requires a monthly premium, which is deducted from your Social Security benefits. There are also deductibles and coinsurance costs associated with both Part A and Part B. Understanding these costs is crucial for budgeting and avoiding unexpected healthcare expenses.

Medicare Part A covers services like inpatient hospital care, including a semi-private room, nursing care, hospital meals, lab tests, and surgery. It also covers a limited stay in a skilled nursing facility following a hospital stay, some home health care, and hospice care. Medicare Part B, on the other hand, covers services like doctor visits, outpatient care, preventive services (like screenings and vaccinations), and some medical equipment like wheelchairs and walkers. Think of Part B as your coverage for the everyday healthcare needs that keep you healthy.

Benefits of Medicare Part A and B:

1. Access to Hospital and Medical Care: Medicare Part A and Part B provide access to a wide range of essential medical services. Imagine needing surgery after a fall - Part A covers your hospital stay. Or needing regular check-ups with your physician - Part B has you covered.

2. Financial Protection: While there are costs associated with Medicare, it offers significant financial protection against the high costs of healthcare. Imagine facing a serious illness without insurance - the bills could be devastating. Medicare helps protect you from such scenarios.

3. Peace of Mind: Knowing you have access to necessary healthcare provides peace of mind. This allows you to focus on enjoying your retirement or managing any health challenges, without the added worry of exorbitant medical bills.

Action plan: When you turn 65, you'll want to enroll in Medicare during your Initial Enrollment Period. This is a seven-month window that includes the three months before your 65th birthday, your birth month, and the three months after. Missing this period can lead to penalties. It's crucial to research your options and understand your needs to make informed decisions about your coverage.

Advantages and Disadvantages of Medicare Part A and Part B

| Medicare Part | Advantages | Disadvantages |

|---|---|---|

| Part A | Often premium-free for those who qualify. Covers essential hospital services. | Deductibles and coinsurance costs can apply. Doesn’t cover all healthcare needs. |

| Part B | Covers medically necessary services and preventive care. Offers a broad range of outpatient services. | Requires a monthly premium. Has deductibles, coinsurance, and copayments. |

Best Practices:

1. Understand your coverage needs. Consider your health status and anticipated healthcare needs to choose the right plan.

2. Review your Medicare Summary Notice (MSN). This helps track your healthcare utilization and costs.

3. Compare Medicare Supplement plans (Medigap) if you need additional coverage. These plans help cover costs that Original Medicare doesn't.

4. Explore Medicare Advantage plans as an alternative to Original Medicare. These plans often include extra benefits like prescription drug coverage.

5. Stay informed about changes to Medicare. Review your coverage annually to ensure it still meets your needs.

FAQs:

1. What is the difference between Medicare Part A and Medicare Part B? (Part A covers hospital insurance, Part B covers medical insurance).

2. How do I enroll in Medicare Part A and Part B? (You can enroll online, by phone, or in person at a Social Security office).

3. What are the costs associated with Medicare Part A and Part B? (Part A often has no premium, but there are deductibles and coinsurance. Part B has a monthly premium, deductible, and coinsurance).

4. When can I enroll in Medicare Part A and Part B? (Typically during the Initial Enrollment Period around your 65th birthday).

5. What is Medicare Supplement insurance (Medigap)? (Helps cover out-of-pocket costs not covered by Original Medicare).

6. What is Medicare Advantage? (An alternative to Original Medicare offered by private companies).

7. What are the late enrollment penalties? (Penalties added to your premium for enrolling late).

8. Where can I get more information about Medicare? (Medicare.gov, your local Social Security office).

Navigating Medicare can feel like a complex maze, but understanding the basics of Medicare Part A and Medicare Part B is the key to unlocking its benefits. Armed with the right knowledge, you can confidently make informed decisions about your healthcare coverage, protect your financial well-being, and enjoy a healthier, more secure future. Start by reviewing your current health status and predicted future needs. Then explore the various Medicare options available and seek personalized advice if needed. Don't wait – take control of your healthcare journey today!

Ea sports fc 24 xbox one price breakdown

Timeless elegance navigating formal fashion for women over 60

Unlocking albany airports enterprise potential your business travel guide

medicare part a and b | Solidarios Con Garzon

medicare part a and b | Solidarios Con Garzon

2024 Medicare Part B Premiums Jump 59 | Solidarios Con Garzon

Medicare Fee Schedule 2024 Part B | Solidarios Con Garzon

Medicare Announces 2023 Medicare Cost | Solidarios Con Garzon

medicare part a and b | Solidarios Con Garzon

Medicare Part B For 2024 | Solidarios Con Garzon

Medicare Irmaa Brackets 2024 Calculator | Solidarios Con Garzon

Medicare Premiums and Deductibles for 2012 | Solidarios Con Garzon

2024 Medicare Parts A B Premiums and Deductibles | Solidarios Con Garzon

Medicare Part B Coverage | Solidarios Con Garzon

Medicare Deductible For 2024 Update | Solidarios Con Garzon

What Is The 2024 Medicare Premium Part B | Solidarios Con Garzon

medicare part a and b | Solidarios Con Garzon

Medicare 2024 Part B Irmaa | Solidarios Con Garzon